Ocean Newsletter

No.603 March 20, 2026

-

The Future Ocean Sleeping Beneath the Ice: A New World Opened Up by Antarctic RINGS

-

Carbon Cycle Study in the Southern Ocean and a Long-Standing Challenge

-

Arctic Challenge for Sustainability III (ArCS III)

-

The Northern Sea Route: Is the economic model viable?

The Northern Sea Route: Is the economic model viable?

KEYWORDS

Northern Sea Route (NSR) / Maritime Shipping / Russian Arctic Policy

Arild Moe (Senior Research professor, Fridtjof Nansen Institute)

The Northern Sea Route (NSR) has the potential to shorten sailing times between East and West, yet the economic model underpinning its development faces serious challenges. Russia has promoted the development of the route in conjunction with Arctic resource projects; however, Western sanctions and fiscal constraints have rendered future investment prospects increasingly uncertain. Although transport between Russia and China has expanded in recent years, broader utilization by the international shipping industry and the securing of sustainable financing remain difficult.

The Economic Model Underpinning the Development of the Northern Sea Route (NSR)

In recent years renewed attention have been devoted to the possibilities and prospects for Arctic shipping. Navigation routes between East and West that cut sailing time by weeks compared with southern alternatives remain attractive. But what is actually happening on the Northern Sea Route (NSR), and what are the main challenges to further development of this sea route?

The NSR constitutes the section of the Northeast Passage between Novaya Zemlya in the west and the Bering Strait in the east where Russia has established a special regime for administration of shipping. The route ties the country’s northern regions together and provides access to the extensive river systems of Siberia, opening a vast resource potential. It is vital for supplies to communities along the coast.

The Arctic is widely considered a cornerstone of Russia’s economic future. Yet developing and using the route is costly. When the Russian government in 2022 presented its development plan for the NSR up to 2035, total investment needs were estimated at 1.79 trillion rubles—around USD 24 billion at the time. The plan encompassed icebreakers, port infrastructure, extensive dredging and hydrographic work, new rail connections, satellite communication systems, and expanded rescue and salvage capacities. Altogether, the program was broken down into 1,840 individual elements.

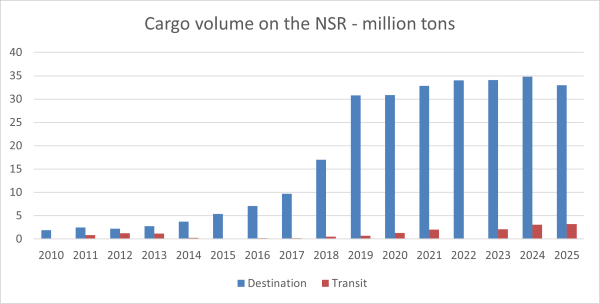

The development of the route was expected to proceed in tandem with major natural resource projects along the Arctic coast—primarily oil and liquefied natural gas, but also coal, minerals, and metals. These industrial projects rely on the NSR both for the delivery of materials and equipment in the construction phase, and to transport output to world markets once production starts – so called destination shipping. The cargo volume on the NSR increased sharply after the start-up of two major hydrocarbon projects, Novy Port oil (2016) and Yamal LNG (2017).

Cargo volumes were, however, projected to grow further and reach 150 million tons in 2030 and 220 million tons in 2035, up from 34 million tons in 2021.

The producers of all this cargo—the users of the sea route— were expected to fund about 40 percent of the infrastructure costs in the development plan. The remaining 60 percent was supposed to be covered by the federal budget and unspecified state sources.

In other words, the economic model for developing the NSR is built on the interdependence between extraction projects and shipping, combined with the state’s ability to invest in the Arctic for long-term national gain. The question is whether this model is still viable.

The NSR constitutes the section of the Northeast Passage between Novaya Zemlya in the west and the Bering Strait in the east where Russia has established a special regime for administration of shipping. The route ties the country’s northern regions together and provides access to the extensive river systems of Siberia, opening a vast resource potential. It is vital for supplies to communities along the coast.

The Arctic is widely considered a cornerstone of Russia’s economic future. Yet developing and using the route is costly. When the Russian government in 2022 presented its development plan for the NSR up to 2035, total investment needs were estimated at 1.79 trillion rubles—around USD 24 billion at the time. The plan encompassed icebreakers, port infrastructure, extensive dredging and hydrographic work, new rail connections, satellite communication systems, and expanded rescue and salvage capacities. Altogether, the program was broken down into 1,840 individual elements.

The development of the route was expected to proceed in tandem with major natural resource projects along the Arctic coast—primarily oil and liquefied natural gas, but also coal, minerals, and metals. These industrial projects rely on the NSR both for the delivery of materials and equipment in the construction phase, and to transport output to world markets once production starts – so called destination shipping. The cargo volume on the NSR increased sharply after the start-up of two major hydrocarbon projects, Novy Port oil (2016) and Yamal LNG (2017).

Cargo volumes were, however, projected to grow further and reach 150 million tons in 2030 and 220 million tons in 2035, up from 34 million tons in 2021.

The producers of all this cargo—the users of the sea route— were expected to fund about 40 percent of the infrastructure costs in the development plan. The remaining 60 percent was supposed to be covered by the federal budget and unspecified state sources.

In other words, the economic model for developing the NSR is built on the interdependence between extraction projects and shipping, combined with the state’s ability to invest in the Arctic for long-term national gain. The question is whether this model is still viable.

Challenges Arising from Sanctions and Fiscal Constraints

Western sanctions have so far not affected exports from the operational Yamal LNG project, but further LNG development is uncertain due to technology sanctions and restricted market access. Even after an end to the war in Ukraine, uncertainty will linger. This will weaken the attractiveness of investments in new Russian LNG projects. The key new oil project has already been delayed, and even if production begins, the necessary ice-strengthened tankers have not been built. In sum, the resource sector’s ability to help finance the NSR has lessened. Besides, a mechanism to integrate infrastructure development costs in the planning of resource extraction projects has not been established. Just recently, Rosatom, the agency responsible for NSR development, proposed a special “investment fee” on cargo owners to finance icebreaker construction. But raising costs for cargo owners now risks further undermining the already strained profitability of some projects.

The federal budget’s capacity is also highly questionable. War-related expenditures are straining public finances, and revenues from Russia’s two crucial export commodities—oil and gas—are declining. In the federal budget for 2026 and the planning period 2027–28, NSR allocations are reduced compared with earlier announcements. It is increasingly clear that the investment program lacks sufficient funding.

In current government documents the expected growth in cargo volume on the NSR is adjusted compared to the 2022 plan, but it is still remarkably high and seems unrealistic. Investment plans have been almost untouched, until very recently. This means that NSR’s financial problems are just becoming more severe. If growth in Arctic oil and gas production continues to be delayed, it seems likely that investment ambitions, including icebreaker construction, will have to be scaled back.

Where, then, does international transit traffic fit in? Before Russia’s full-scale invasion of Ukraine, international transits were few. The big container shipping companies found navigation unpredictable and seasonal, there were draft limitations and lack of ports and markets along the route. For these and other reasons they did not believe the NSR would play any significant role. The Russian position was that international traffic would blossom only once the route had been further developed and services improved, particularly with the establishment of year-round navigation.

The federal budget’s capacity is also highly questionable. War-related expenditures are straining public finances, and revenues from Russia’s two crucial export commodities—oil and gas—are declining. In the federal budget for 2026 and the planning period 2027–28, NSR allocations are reduced compared with earlier announcements. It is increasingly clear that the investment program lacks sufficient funding.

In current government documents the expected growth in cargo volume on the NSR is adjusted compared to the 2022 plan, but it is still remarkably high and seems unrealistic. Investment plans have been almost untouched, until very recently. This means that NSR’s financial problems are just becoming more severe. If growth in Arctic oil and gas production continues to be delayed, it seems likely that investment ambitions, including icebreaker construction, will have to be scaled back.

Where, then, does international transit traffic fit in? Before Russia’s full-scale invasion of Ukraine, international transits were few. The big container shipping companies found navigation unpredictable and seasonal, there were draft limitations and lack of ports and markets along the route. For these and other reasons they did not believe the NSR would play any significant role. The Russian position was that international traffic would blossom only once the route had been further developed and services improved, particularly with the establishment of year-round navigation.

■A 60-megawatt Russian icebreaker assisting a cargo vessel. (Photo credit: Rosatom)

■LNG loading operations at Yamal. (Photo credit: Novatek)

The Current State and Future Prospects of International Transit

In 2022, international transits stopped completely. But in the last two years record-high transit shipping has been reported, around 3.2 million tons in 2025. However, almost all of this “transit” is between China and Russia. It is classified as transit because ships cross both the eastern and western boundaries of the NSR. Oil dominates the cargo, some 1.9 million tons in 2025, according to Centre for High North Logistics. Since 2023, some Russian oil has been shipped from Baltic and Murmansk terminals to China via the Arctic—a result of sanctions on Russian seaborne oil exports to Europe, its traditional market. The NSR offers an alternative to the Suez Canal or the route around Africa, but it is only relevant as long as sanctions are in place. Coal exports also make up a substantial share of the NSR traffic with China.

The past three years have also seen growing activity with smaller container vessels and general cargo ships. Typically, industrial goods are shipped from ports in south-east China for unloading in Arkhangelsk or the St. Petersburg region. About twenty such port calls took place in 2025. In October 2025, a genuine international transit occurred when a large container ship travelled from China to a port in England without stopping in Russia. Chinese companies running these operations have identified a niche they believe can expand and they have announced plans to increase activity. Russia actively promotes the China trade as evidence of international interest in NSR transit.

International users were never expected to play a significant role in financing NSR development; they were only to cover part of operational costs, such as icebreaker assistance. In recent years, Russian officials have even acknowledged that subsidizing international transit—including China-related traffic—is necessary to make the route competitive. This is hardly a sustainable solution. There is little indication that the broader international shipping industry has changed its view. If anything, uncertainties stemming from the war in Ukraine have heightened the perceived risks of long-term investment in Russia or in vessels tied to NSR operations. Yet, long-term investment is precisely what the Russian Arctic requires.

The past three years have also seen growing activity with smaller container vessels and general cargo ships. Typically, industrial goods are shipped from ports in south-east China for unloading in Arkhangelsk or the St. Petersburg region. About twenty such port calls took place in 2025. In October 2025, a genuine international transit occurred when a large container ship travelled from China to a port in England without stopping in Russia. Chinese companies running these operations have identified a niche they believe can expand and they have announced plans to increase activity. Russia actively promotes the China trade as evidence of international interest in NSR transit.

International users were never expected to play a significant role in financing NSR development; they were only to cover part of operational costs, such as icebreaker assistance. In recent years, Russian officials have even acknowledged that subsidizing international transit—including China-related traffic—is necessary to make the route competitive. This is hardly a sustainable solution. There is little indication that the broader international shipping industry has changed its view. If anything, uncertainties stemming from the war in Ukraine have heightened the perceived risks of long-term investment in Russia or in vessels tied to NSR operations. Yet, long-term investment is precisely what the Russian Arctic requires.

■Cargo volume on the Northern Sea Route (million tons)