Introduction

The surprise attack on Iran by the United States and Israel on February 28, 2026, triggered a rapid escalation of Iranian military activity across the Persian Gulf. Retaliatory strikes damaged not only US military facilities but also oil and gas infrastructure, effectively shutting down the Strait of Hormuz.

For the Gulf oil producers, hydrocarbon revenues are the central pillar of fiscal stability, and any sustained decline directly worsens their fiscal positions. At the same time, the slowdown in dollar inflows from energy exports threatens to weaken the long standing pattern in which surplus petrodollars cycle back into US financial markets—a core mechanism binding the Gulf states to the United States.

This paper examines how the Iran war is affecting Gulf energy exports and revenues. It also considers how a prolonged decline in hydrocarbon income—and the resulting slowdown in dollar recycling—could reshape the financial relationship between the Gulf oil producers and the United States.

The Effective Closure of Hormuz

The sudden deterioration of the regional security environment has effectively closed the Strait of Hormuz—through which massive volumes of crude oil and liquefied natural gas (LNG) had been transiting daily. On March 2, Iran’s Islamic Revolutionary Guard Corps warned vessels against transiting the strait.[1] Later that day, major marine insurers announced they would suspend war risk coverage for ships entering the Persian Gulf beginning March 5.[2] Faced with direct Iranian threats and the loss of insurance coverage, shipping and trading companies have sharply reduced traffic. As a result, vessel transits through Hormuz plunged from 95 on February 27 (the day before the US-Israeli attack) to just 17 on March 1 and have since remained in the single digits.[3]

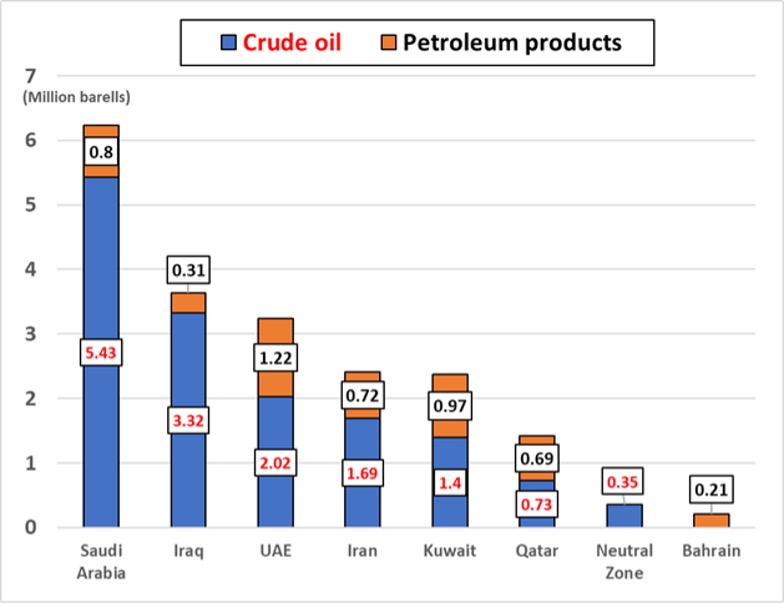

The implications are enormous. Hormuz is the main export route for crude oil and refined petroleum products from Saudi Arabia, Iraq, the United Arab Emirates, Iran, Kuwait, Qatar, Bahrain, and the Saudi-Kuwaiti Neutral Zone. In 2025, 14.94 million barrels per day (bpd) of crude oil—roughly 34% of global seaborne trade—and 4.92 million bpd of refined products transited the strait, largely bound for Asian markets (Figure 1). Nearly all LNG exports from Qatar and the UAE (except those destined for Kuwait) also pass through Hormuz; in 2025, LNG shipments via the strait accounted for about 20% of global LNG trade.

Figure 1. Exports of Crude Oil and Refined Products via the Strait of Hormuz in 2025

Although there are alternative routes that bypass Hormuz, including several pipelines, their capacity is insufficient to offset the disruption. Saudi Arabia’s East-West Pipeline linking Abqaiq to Yanbu can move 5 million to 7 million bpd; the UAE’s Abu Dhabi Crude Oil Pipeline from Habshan to Fujairah can transport 1.8 million bpd; and Iran’s Goreh-Jask pipeline, completed in 2021, adds another 300,000 bpd.[5]

Even assuming maximum utilization of Saudi and Emirati lines (8.8 million bpd), though, these routes cannot compensate for the roughly 20 million bpd that normally transit Hormuz.

Production Cuts and Damage to Energy Infrastructure

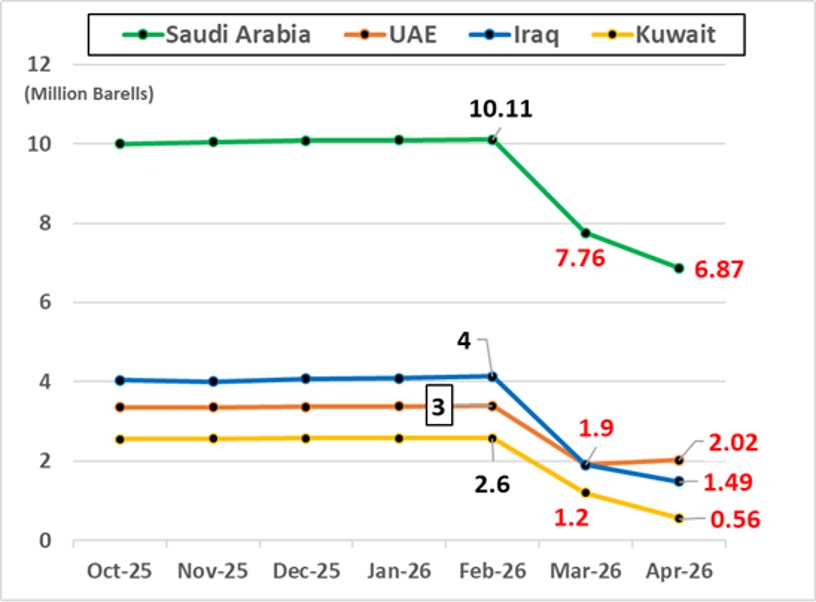

Since the outbreak of the war, Gulf oil producers have been unable to export as before. While some crude can be temporarily stored domestically, capacity is limited, forcing producers to reduce output. Between February and April 2026, Saudi Arabia cut crude production from 10.11 million to 6.87 million bpd; Iraq from 4.14 million to 1.49 million bpd; the UAE from 3.39 million to 2.02 million bpd; and Kuwait from 2.58 million to 560,000 bpd (Figure 2). Combined, the four states lost 9.28 million bpd of production. Thus, the closure of Hormuz has depressed not only exports but also the region’s production capacity.

Figure 2. Daily Crude Oil Production in Saudi Arabia, the UAE, Iraq, and Kuwait

Beyond the chokepoint itself, Iranian retaliatory strikes have increasingly targeted Gulf energy infrastructure. Even if navigation through Hormuz resumes, damage to oil and gas facilities could constrain Gulf export capacity for years.

Each time Iran has come under attack from the United States and Israel, it has responded with drone and missile strikes across the Gulf. The targets have expanded beyond US military facilities to include airports, ports, industrial zones, residential areas, and—critically—energy infrastructure.

The biggest damage to date has been to Qatar’s LNG sector. On the night of March 18 and the early hours of March 19, Iran launched missile strikes on the Ras Laffan Industrial City, damaging Trains 4 and 6 of the RasGas LNG project. Both units are joint ventures between QatarEnergy and ExxonMobil. With 2 of Qatar’s 14 LNG trains knocked offline, the country has lost 12.8 million tons per year of production capacity—roughly 17% of its exports—representing an estimated annual revenue loss of $20 billion. Repairs are expected to take three to five years.[7]

As a result, Qatar’s total LNG production capacity is set to decline over the long term, falling from 77.0 million tons per year to around 64.2 million tons. The attacks have also delayed the first phase of Qatar’s long‑planned LNG expansion—the North Field East project (32 million tons per year)—pushing its expected start date from November 2026 to sometime in 2027–28.[8]

Iran has also struck refined product facilities across the Gulf, including Saudi Arabia’s Ras Tanura and Samref refineries; Kuwait’s Mina al Ahmadi and Mina Abdullah refineries; the UAE’s Ruwais refinery; and Bahrain’s Sitra refinery. In Qatar, the Pearl GTL (gas to liquids) plant—operated by Shell—was also hit and is expected to remain offline for at least a year. The shutdown will eliminate roughly 18.6 million barrels of condensate exports (24% of Qatar’s total), 1.281 million tons of liquefied petroleum gas (13%), and 594,000 tons of naphtha (6%).[9]

Taken together, the shutdown of the strait, the production cuts forced on regional producers, and the damage inflicted on energy infrastructure have all destabilized the Gulf states’ resource revenues. Global oil prices have risen since the start of the war, a development that would normally boost export earnings. But because of constraints on export routes, reduced output, and the impact of infrastructure damage, many Gulf producers have not benefitted from higher prices.

According to Reuters estimates, March 2026 oil revenues diverged sharply across the region depending on reliance on Hormuz and availability of alternative routes. Iran, Oman, and Saudi Arabia saw revenue increases—of $1.54 billion, $610 million, and $560 million year on year, respectively—thanks to partial use of non Hormuz routes and higher prices. By contrast, the UAE, Qatar, Kuwait, and Iraq suffered losses. The UAE’s declines were limited to $170 million due to its pipeline, but Iraq, Kuwait, and Qatar—lacking viable alternatives—lost an estimated $5.53 billion, $2.39 billion, and $1.15 billion, respectively.[10]

Gas revenues have been hit even harder. LNG shipments from Qatar and the UAE rely on specialized carriers that must transit Hormuz. Before the war, roughly three LNG tankers per day departed the Gulf.[11] By mid May—two and a half months into the conflict—only two LNG carriers had departed from Qatar and two from the UAE.[12]

Implications for Gulf-US Financial Relations

The Iran war threatens not only hydrocarbon revenues but also the financial architecture that has long underpinned the Gulf states’ relations with the United States—most notably the petrodollar system and the dollar peg regimes.

The petrodollar system refers to the practice of Gulf producers selling oil in US dollars and recycling surplus revenues into dollar denominated assets, such as US Treasuries, equities, bank deposits, and US made weapons.[13]

Since the 1970s, this arrangement has rested on a strategic bargain: the United States provides security, and the Gulf states maintain dollar based oil trade and large dollar holdings.[14] The Iran war, though, has raised doubts about Washington’s ability to protect Gulf shipping lanes and critical infrastructure. As a result, the core components of exchange—US security guarantees in return for dollar based energy trade—are now under strain.

The Gulf states also maintain dollar pegged exchange rate regimes, which help stabilize oil revenues, import payments, and financial markets.[15] Maintaining the peg requires substantial dollar reserves to defend their currencies during periods of capital outflow. But with energy exports disrupted and reconstruction and defense costs rising, governments may be forced to draw down sovereign wealth funds and foreign exchange reserves to support their domestic economies. As more dollars are diverted to crisis response rather than invested abroad, the cost of maintaining the peg becomes more salient, potentially prompting future debate over exchange rate reform.

A sustained reduction in Gulf purchases of US assets would weaken the flow of petrodollars into US financial markets—undermining Treasury financing and the broader foundations of dollar hegemony.

Amid concerns about de dollarization, the UAE stands out for seeking to deepen its financial ties with the United States. Abu Dhabi is currently negotiating a bilateral currency swap agreement with Washington. Swap lines allow a partner central bank to obtain dollars during market stress and supply them to domestic institutions. Given the UAE’s vast sovereign wealth assets [16] Amid concerns about de dollarization, the UAE stands out for seeking to deepen its financial ties with the United States. Abu Dhabi is currently negotiating a bilateral currency swap agreement with Washington. Swap lines allow a partner central bank to obtain dollars during market stress and supply them to domestic institutions. Given the UAE’s vast sovereign wealth assets [17] US officials, for their part, view expanding swap line coverage into the Gulf and Asia as a way to reinforce the dollar’s international role and counter emerging alternative payment systems.[18]

The UAE’s effort to strengthen ties with Washington extends beyond security cooperation [19] into the financial domain. Its April 2026 decision to withdraw from OPEC and pursue higher oil production also aligns, to some extent, with US preferences for stable oil prices. These moves reflect a broader strategy: as a small state, the UAE seeks to maximize its security and international influence by embedding itself more deeply within US led financial and geopolitical structures.

(2026/06/09)

Notes

- 1 “Iran vows to attack any ship trying to pass through Strait of Hormuz,” Reuters, March 3, 2026.

- 2 Weilun Soon, Alex Longley, and Leonard Kehnscherper, “Insurance Clubs to Halt Ship War-Risk Cover in Persian Gulf,” Bloomberg, March 2, 2026.

- 3 “Port Monitor: Strait of Hormuz,” IMF Portwatch, accessed May 12, 2026.

- 4 International Energy Agency, “Strait of Hormuz Factsheet,” February 2026.

- 5 “Amid regional conflict, the Strait of Hormuz remains critical oil chokepoint,” U.S. Energy Information Administration, June 16, 2025.

- 6 “OPEC Monthly Oil Market Report January 2026,” Organization of the Petroleum Exporting Countries (OPEC), January 14, 2026, p.54; “OPEC Monthly Oil Market Report April 2026,” OPEC, April 13, 2026, p.51; “OPEC Monthly Oil Market Report May 2026,” OPEC, May 13, 2026, p.53.

- 7 “H.E. Minister Saad Sherida Al-Kaabi: The missile attacks reduced Qatar’s LNG export capacity by 17% and caused an estimated loss of $20 billion in annual revenue,” QatarEnergy, March 19, 2026.

- 8 “Ras Laffan attacks fundamentally reshape global LNG outlook as recovery timeline likely significantly extended,” Wood Mackenzie, March 19, 2026.

- 9 QatarEnergy, March 19, 2026 (see note 7).

- 10 Ahmad Ghaddar and Yousef Saba, “Hormuz closure divides the fortunes of Middle Eastern oil states,” Reuters, April 7, 2026.

- 11 Stephen Stapczynski and Weilun Soon, “Qatar Sends First LNG Shipment Through Hormuz Since War Started,” Bloomberg, May 10, 2026.

- 12 “Second ADNOC LNG tanker crosses Strait of Hormuz amid Iran war, ship-tracking data shows,” Reuters, May 6, 2026; Marwa Rashad, “Second Qatari LNG tanker successfully crosses Hormuz to Pakistan as Iran war continues, data shows,” Reuters, May 13, 2026.

- 13 Mike Dolan, “Iran war rattles Gulf petrodollar foundations,” Reuters, March 25, 2026.

- 14 In the early 1970s, the US economy was reeling from the fiscal burdens and inflation associated with the Vietnam War, compounded by the severe shock of the 1973 oil crisis. The Nixon administration therefore sought a framework that would both limit the risk of oil being used as an “economic weapon” and channel the oil producers’ surplus revenues back into the United States. In 1974, Treasury Secretary William Simon negotiated with Saudi Arabia to establish an arrangement under which the United States would provide security guarantees in exchange for Saudi Arabia reinvesting its oil revenues in US Treasury securities. Andrea Wong, “The Untold Story Behind Saudi Arabia’s 41-Year U.S. Debt Secret,” Bloomberg, May 31, 2016.

- 15 According to the IMF, Saudi Arabia, the UAE, Qatar, Oman, and Bahrain are classified as maintaining a “conventional peg” with the US dollar as the anchor currency, effectively operating dollar peg regimes. Kuwait, by contrast, pegs its currency not to the US dollar alone but to an undisclosed basket of currencies. Annual Report on Exchange Arrangements and Exchange Restrictions 2022, IMF, July 26, 2023, p. 14.

- 16 According to the latest estimates published by the Sovereign Wealth Fund Institute, the combined assets of the UAE’s major sovereign wealth funds—the Abu Dhabi Investment Authority, Investment Corporation of Dubai, Mubadala Investment Company, Abu Dhabi Developmental Holding Company, and the Emirates Investment Authority—amount to roughly $2.3 trillion. “List of 32 Sovereign Wealth Fund Profiles in Middle East,” Sovereign Wealth Fund Institute, accessed May 17, 2026.

- 17 Daniel Flatley and Enda Curran, “How the US Is Using Swap Lines to Project Financial Power,” Bloomberg, May 5, 2026.

- 18 Treasury Secretary Scott Bessent (@SecScottBessent), X post, April 24, 2026.

- 19 Amid the Iran war, the UAE has been deepening its security cooperation with the United States. On March 19, 2026, the Department of State approved more than $8.4 billion in foreign military sales to the UAE, including a long range identification radar for the THAAD system, Fixed Site Low, Slow, Small Unmanned Aircraft System Integrated Defeat System (FS LIDS) units, AMRAAM medium range air to air missiles, and equipment and upgrades related to the F 16 fighter aircraft. “Foreign Military Sales notices on UAE arms sales,” US Department of State, March 19, 2026.